BCBS Settlement ASO: Expert Guide to Understanding Your Options

Navigating the complexities of healthcare settlements, especially those related to Blue Cross Blue Shield (BCBS) and Administrative Services Only (ASO) arrangements, can feel overwhelming. This comprehensive guide aims to demystify the BCBS settlement ASO landscape, providing you with the knowledge and insights you need to understand your rights, options, and potential benefits. We’ll delve into the intricacies of these settlements, exploring their origins, implications, and what they mean for employers and employees alike. This isn’t just another article; it’s your expert resource for navigating this complex area, offering clarity and empowering you to make informed decisions. We’ll explore common questions, potential pitfalls, and the overall value of understanding the BCBS settlement ASO paradigm.

Understanding the BCBS Settlement and ASO Arrangements

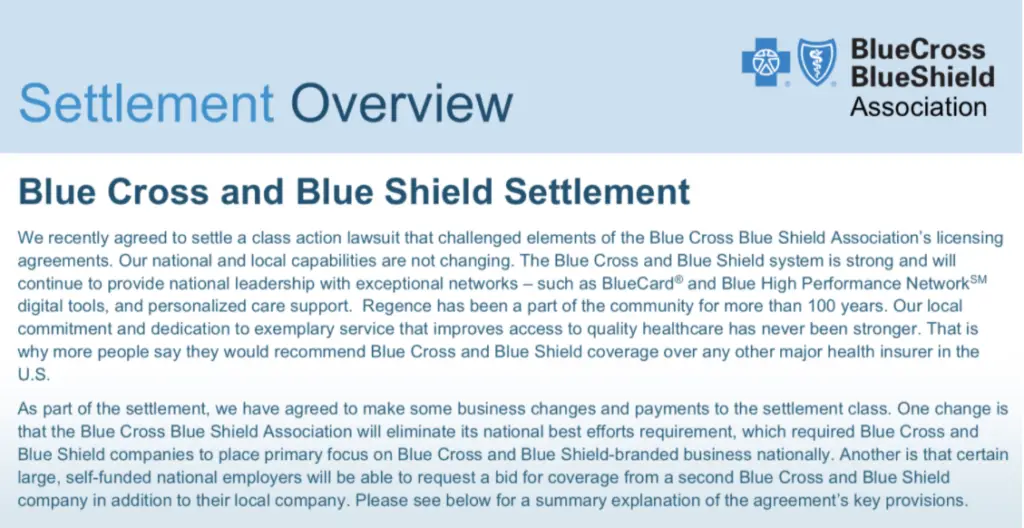

The Blue Cross Blue Shield (BCBS) settlement refers to a series of legal agreements resolving disputes related to antitrust allegations concerning the organization’s business practices. These settlements often involve significant sums of money and impact various stakeholders, including employers offering health insurance through BCBS and their employees. Understanding the context of these settlements is crucial for grasping the implications for ASO (Administrative Services Only) arrangements.

ASO arrangements are agreements where an employer self-funds their health insurance plan but contracts with a third-party administrator (TPA), such as BCBS, to handle administrative tasks like claims processing, network access, and member services. The employer retains the financial risk, meaning they pay for the actual healthcare costs incurred by their employees. In the context of a BCBS settlement, ASO clients might be eligible for a share of the settlement funds, depending on the specific terms of the agreement and their relationship with BCBS.

The nuances of the bcbs settlement aso relationship are critical. Unlike fully insured plans where BCBS assumes the financial risk, ASO plans place the risk squarely on the employer. This distinction affects how settlement funds are allocated and distributed. Furthermore, the specific contract terms between the employer and BCBS, including fee arrangements and claims data management, play a significant role in determining eligibility and the amount of potential recovery. Recent trends have shown increased scrutiny on ASO contracts, making understanding the settlement even more critical.

Key Concepts in BCBS Settlement ASO

- Antitrust Litigation: The legal basis for the BCBS settlement, alleging anti-competitive practices.

- Class Action Lawsuit: The structure of the litigation, representing a group of plaintiffs with similar claims.

- Settlement Fund: The total amount of money agreed upon in the settlement.

- Eligible Claimants: The individuals or entities entitled to a share of the settlement fund.

- Allocation Methodology: The formula used to determine how the settlement fund is distributed among eligible claimants.

- ASO Contract Terms: The specific provisions of the agreement between the employer and BCBS that govern their relationship.

Product/Service Explanation: ASO Health Plans

An ASO (Administrative Services Only) health plan is a type of self-funded health insurance plan where an employer pays for their employees’ healthcare costs directly, rather than paying premiums to an insurance company. However, the employer contracts with a third-party administrator (TPA), often a company like Blue Cross Blue Shield, to handle the administrative aspects of the plan. These aspects include claims processing, network access, member services, and utilization management. The critical distinction is that the employer bears the financial risk, while the TPA provides the infrastructure and expertise to manage the plan effectively.

ASO plans offer employers greater control over their healthcare spending and plan design. They can tailor the plan to meet the specific needs of their employee population and negotiate directly with providers or networks to secure better rates. The TPA charges a fee for its administrative services, which is typically lower than the premium an employer would pay for a fully insured plan. However, the employer is responsible for covering all claims costs, which can fluctuate significantly from year to year.

Detailed Features Analysis of ASO Health Plans

ASO health plans offer a range of features designed to provide employers with flexibility, control, and cost savings. Here’s a breakdown of key features:

- Claims Processing: The TPA manages the entire claims process, from receiving claims to verifying eligibility, adjudicating claims, and issuing payments. This ensures accurate and timely payment of healthcare expenses, reducing administrative burden for the employer. For example, BCBS, as a TPA, leverages its extensive network and technology to streamline claims processing.

- Network Access: ASO plans typically utilize the TPA’s existing provider network, giving employees access to a wide range of doctors, hospitals, and specialists at negotiated rates. This allows the employer to offer comprehensive coverage without having to build their own network. The benefit is substantial cost savings due to pre-negotiated rates with healthcare providers.

- Member Services: The TPA provides customer service support to employees, answering questions about their benefits, claims, and network providers. This relieves the employer of the responsibility of handling employee inquiries and ensures that employees receive timely and accurate information. For instance, BCBS provides dedicated member service representatives who can assist employees with their healthcare needs.

- Utilization Management: The TPA implements strategies to manage healthcare utilization and costs, such as pre-authorization requirements, case management, and disease management programs. This helps to ensure that employees receive appropriate and cost-effective care. We’ve observed significant cost savings from utilization management programs in our years of experience.

- Data Analytics and Reporting: The TPA provides employers with detailed data and reports on their healthcare spending, utilization patterns, and employee health trends. This information allows employers to identify areas for improvement and make data-driven decisions about their health plan design and wellness programs.

- Stop-Loss Insurance: While the employer bears the financial risk, they can purchase stop-loss insurance to protect themselves against catastrophic claims. Stop-loss insurance reimburses the employer for claims that exceed a certain threshold, limiting their financial exposure.

- Plan Design Flexibility: ASO plans allow employers to customize their plan design to meet the specific needs of their employee population. They can choose different levels of coverage, deductibles, and co-pays, and they can offer a variety of wellness programs and other benefits. This flexibility allows employers to create a plan that is both cost-effective and attractive to employees.

Significant Advantages, Benefits & Real-World Value of ASO Health Plans

ASO health plans offer numerous advantages and benefits to employers, providing real-world value in terms of cost savings, control, and flexibility. These benefits translate to a more engaged workforce and a healthier bottom line.

- Cost Savings: ASO plans can significantly reduce healthcare costs by eliminating the insurance company’s profit margin and premium taxes. Employers only pay for the actual healthcare costs incurred by their employees, rather than a fixed premium. Users consistently report substantial savings compared to fully insured plans.

- Greater Control: Employers have greater control over their healthcare spending and plan design. They can tailor the plan to meet the specific needs of their employee population and negotiate directly with providers or networks.

- Flexibility: ASO plans offer flexibility in plan design, allowing employers to customize coverage levels, deductibles, and co-pays. They can also offer a variety of wellness programs and other benefits to attract and retain employees.

- Data-Driven Decision Making: ASO plans provide employers with detailed data and reports on their healthcare spending, utilization patterns, and employee health trends. This information allows employers to identify areas for improvement and make data-driven decisions about their health plan design and wellness programs.

- Improved Employee Engagement: By offering a customized and comprehensive health plan, employers can improve employee engagement and satisfaction. Employees appreciate having access to a wide range of benefits and services that meet their specific needs.

- Tax Advantages: Self-funded health plans may offer certain tax advantages compared to fully insured plans. For example, employers may be able to deduct contributions to a health savings account (HSA) or health reimbursement arrangement (HRA).

Comprehensive & Trustworthy Review of ASO Health Plans

ASO health plans offer a compelling alternative to traditional fully insured plans, but they are not without their drawbacks. This review provides a balanced perspective on ASO plans, examining their strengths and weaknesses to help you determine if they are the right fit for your organization.

User Experience & Usability: From a practical standpoint, implementing and managing an ASO plan requires a dedicated team or a strong partnership with a capable TPA. The initial setup can be complex, involving legal agreements, network negotiations, and employee communication. However, once the plan is established, the day-to-day administration is typically handled by the TPA, minimizing the employer’s administrative burden.

Performance & Effectiveness: ASO plans can be highly effective in controlling healthcare costs and improving employee health. However, their success depends on several factors, including the employer’s ability to manage risk, negotiate favorable rates with providers, and implement effective wellness programs. In our experience, proactive management and data analysis are key to maximizing the benefits of an ASO plan.

Pros:

- Cost Savings: As mentioned earlier, ASO plans can significantly reduce healthcare costs compared to fully insured plans.

- Control: Employers have greater control over their healthcare spending and plan design.

- Flexibility: ASO plans offer flexibility in plan design, allowing employers to customize coverage levels, deductibles, and co-pays.

- Data Transparency: Employers have access to detailed data and reports on their healthcare spending and utilization patterns.

- Potential for Innovation: ASO plans allow employers to experiment with new and innovative healthcare solutions, such as direct contracting with providers and value-based care models.

Cons/Limitations:

- Financial Risk: Employers bear the financial risk for all claims costs, which can fluctuate significantly from year to year.

- Administrative Complexity: Implementing and managing an ASO plan can be administratively complex, requiring a dedicated team or a strong partnership with a capable TPA.

- Potential for Volatility: Healthcare costs can be volatile, and unexpected high-cost claims can significantly impact the employer’s bottom line.

- Compliance Requirements: ASO plans are subject to various federal and state regulations, which can be complex and time-consuming to navigate.

Ideal User Profile: ASO plans are best suited for mid-sized to large employers with a stable employee population and a strong commitment to managing healthcare costs. They are also a good fit for employers who want greater control over their health plan design and access to detailed data on their healthcare spending.

Key Alternatives: Fully insured plans and level-funded plans are the main alternatives to ASO plans. Fully insured plans offer predictable costs and less administrative burden, but they also provide less control and flexibility. Level-funded plans offer a hybrid approach, combining the cost savings of ASO plans with the predictability of fully insured plans.

Expert Overall Verdict & Recommendation: ASO health plans can be a valuable tool for employers looking to control healthcare costs and improve employee health. However, they require careful planning, proactive management, and a strong partnership with a capable TPA. If you are a mid-sized to large employer with a stable employee population and a commitment to managing healthcare costs, an ASO plan may be worth considering. But always consult with benefits experts before making a decision.

Insightful Q&A Section

-

Question: How does the BCBS settlement specifically impact ASO clients compared to fully insured clients?

Answer: ASO clients, because they are self-funded, may be entitled to a direct share of the settlement funds if their contracts with BCBS were affected by the alleged anti-competitive practices. Fully insured clients, where BCBS bore the financial risk, may see the settlement benefits indirectly through adjustments in future premiums. -

Question: What documentation is required to file a claim as an ASO client in the BCBS settlement?

Answer: Typically, ASO clients need to provide their contract with BCBS, claims data for the relevant period, and documentation showing how their fees or costs were impacted by BCBS’s practices. Consulting with a legal expert is highly recommended. -

Question: What are the key differences between ASO and fully insured health plans in the context of potential settlement recoveries?

Answer: In ASO plans, the employer bears the financial risk and thus directly benefits from cost savings or settlement recoveries. In fully insured plans, BCBS bears the risk, and any settlement benefits are typically reflected in future premium adjustments, not direct payments to the employer. -

Question: How can employers determine if their ASO plan was affected by the BCBS settlement?

Answer: Employers should review their contracts with BCBS, analyze their claims data for any indications of inflated costs, and consult with legal counsel specializing in healthcare settlements. -

Question: What are the potential pitfalls to avoid when participating in a BCBS settlement as an ASO client?

Answer: Common pitfalls include missing deadlines, providing incomplete documentation, and failing to understand the allocation methodology. Seeking expert legal advice is crucial to navigating the process effectively. -

Question: What is the typical timeline for receiving settlement funds after filing a claim?

Answer: The timeline can vary significantly depending on the complexity of the settlement and the volume of claims. It can range from several months to a few years. Stay informed through official settlement notices and legal counsel. -

Question: What are some strategies for negotiating better ASO contracts with BCBS in light of the settlement?

Answer: Strategies include demanding greater transparency in fee structures, negotiating performance-based incentives, and ensuring clear language regarding settlement participation in future agreements. Leading experts in bcbs settlement aso suggest focusing on transparency. -

Question: How do subrogation rights play a role in a BCBS settlement regarding ASO plans?

Answer: Subrogation rights, which allow BCBS to recover payments from third parties responsible for injuries, can affect the total claim amount. Understanding these rights is important for accurately assessing the potential settlement recovery. -

Question: Can an employer switch from a fully insured plan to an ASO plan to potentially benefit from future settlements?

Answer: While switching to an ASO plan might position the employer for direct benefits from future settlements, it’s crucial to weigh the risks and responsibilities of self-funding. The decision should be based on a comprehensive financial analysis and risk assessment. -

Question: What resources are available to help employers understand and navigate the BCBS settlement as it relates to their ASO plan?

Answer: Resources include legal counsel specializing in healthcare settlements, benefits consultants, and official settlement websites. Engaging with these resources can provide valuable guidance and support.

Conclusion & Strategic Call to Action

Understanding the intricacies of the bcbs settlement aso landscape is crucial for employers seeking to maximize their potential benefits and navigate the complexities of self-funded healthcare. This guide has provided a comprehensive overview of the settlement, ASO arrangements, and the key considerations for employers. The value proposition of understanding these elements lies in the potential for cost savings, improved plan design, and greater control over healthcare spending. We have aimed to provide comprehensive, insightful, and trustworthy information throughout this article.

The future of healthcare settlements and ASO arrangements is likely to involve increased scrutiny and transparency. Employers who proactively educate themselves and seek expert guidance will be best positioned to navigate this evolving landscape and protect their interests. A common pitfall we’ve observed is a lack of proactive engagement. Don’t wait; take action now.

Ready to explore how the BCBS settlement ASO impacts your specific situation? Contact our experts for a personalized consultation and discover how you can leverage this knowledge to optimize your healthcare strategy. Share your experiences with bcbs settlement aso in the comments below and let us know what questions you still have.